40-33: Copies of all Stockholder Derivative Actions filed with a court against an Investment Company or an Affiliate thereof [Section 33]

Published on June 26, 2026

|

Eversheds Sutherland (US) LLP 700 Sixth Street, NW, Suite 700 Washington, DC 20001-3980

D: +1 202.383.0218 F: +1 202.637.3593

cynthiakrus@ eversheds-sutherland.com |

June 26, 2026

VIA EDGAR

U.S. Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Re: | Blue Owl Technology Finance Corp. |

File No. 000-55977

Filing Pursuant to Section 33 of the Investment Company Act of 1940

Dear Sir/Madam:

On behalf of Blue Owl Technology Finance Corp. (the “Company”) and certain affiliated persons thereof, and pursuant to Section 33 of the Investment Company Act of 1940, as amended, enclosed for filing please find a copy of the verified complaint filed in the United States District Court for the Southern District of New York in case 1:26-cv-05183 on June 18, 2026 by Martin Siegel and Thomas Kelly, as stockholders of the Company, as plaintiffs, against Blue Owl Technology Credit Advisors LLC, as defendant.

If you have any questions or comments regarding this submission, please do not hesitate to contact Dwaune Dupree (202.383.0206) or me (202.383.0218).

| Sincerely, |

| /s/ Cynthia M. Krus |

Eversheds Sutherland (US) LLP is part of a global legal practice, operating through various separate and distinct legal entities, under Eversheds Sutherland. For a full description of the structure and a list of offices, please visit www.eversheds-sutherland.com.

| Provided by CourtAlert | www.CourtAlert.com |

| UNITED STATES DISTRICT COURT | ||

| SOUTHERN DISTRICT OF NEW YORK

|

||

| MARTIN SIEGEL and THOMAS KELLY, | No. | |

| Plaintiffs, |

VERIFIED COMPLAINT | |

| v. |

||

| BLUE OWL TECHNOLOGY CREDIT | ||

| ADVISORS LLC, | ||

| Defendant.

|

||

Plaintiffs Martin Siegel and Thomas Kelly (“Plaintiffs”), by their undersigned counsel, and as stockholders of Blue Owl Technology Finance Corp. (“OTF”), bring this action against Blue Owl Technology Credit Advisors LLC (“Defendant”) pursuant to Section 36(b) of the Investment Company Act of 1940 (the “ICA”), 15 U.S.C. § 80(a)-35(b) for the benefit of OTF and its stockholders. The following allegations are based on knowledge as to Plaintiffs and Plaintiffs’ own actions, and on information and belief as to all other matters, based on the investigation of Plaintiffs’ counsel, which included, among other things, a review and analysis of documents, including filings with the Securities and Exchange Commission (“SEC”), news reports, and other publicly available materials. Plaintiffs believe that a reasonable opportunity for discovery will yield additional substantial evidentiary support for the allegations herein.

NATURE OF THE ACTION

1. Defendant is the investment adviser of OTF and has systematically inflated the value of OTF’s assets in order to extract windfall fees paid by OTF to Defendant in violation of the ICA.

2. OTF is a specialty finance company treated as a BDC under the ICA and managed by Defendant in return for advisory fees and other fees based on OTF’s portfolio assets. The cost of both the management fee and incentive fee are ultimately borne by OTF’s stockholders such as Plaintiffs.

| Provided by CourtAlert | www.CourtAlert.com |

3. Section 36(b) of the ICA imposes a fiduciary duty on investment advisers to ensure that the compensation they receive from an investment company is not excessive. Defendant breached that fiduciary duty here by receiving investment advisory fees from OTF that are so disproportionately large that they bear no relationship to the value of the services provided by Defendant and could not have been the product of arm’s-length bargaining.

4. Defendant’s fees were grossly excessive because Defendant assigned inflated values to OTF’s assets and investment income and then collected inflated fees based on those inflated valuations. The fee structure set forth in the advisory agreement between OTF and Defendant fosters excessive fees because of the inherent conflict that exists by having Defendant serve as the entity that both values OTF’s assets and chooses its portfolio assets (including assets that ultimately result in fees to Defendant even when those assets are ultimately not realized by OTF).

5. The inflated values assigned to OTF’s portfolio of assets are underscored by numerous public reports that Defendant and its parent, Blue Owl Capital Inc. (“Blue Owl”), have been mismarking and otherwise manipulating the assigned fair value of assets held across a variety of public and private BDCs.1 In March 2026, a Los Angeles-based investment fund reported that another Blue Owl public BDC, Blue Owl Capital Corporation’s (“OBDC”), misrepresented loan loss rates in marketing materials, and were sitting on larger losses than reported, and that Blue Owl assigned higher marks to loans in OBDC’s portfolio compared with current public trading prices

| 1 | See Andrew Bary, Cheap public private-credit funds could mean bigger outflows from private ones, BARRON’S (Apr. 3, 2026), available at http://www.barrons.com/articles/stock-public-private-credit-funds-b7181648. |

2

| Provided by CourtAlert | www.CourtAlert.com |

of the same debt, calling into question the true valuation of OBDC’s portfolio.2 While the investment fund specifically criticized the true valuation of OBDC’s portfolio, all of Blue Owl’s BDCs, including OTF, have a more than 70% portfolio overlap,3 and the specific investments criticized as overvalued are included in OTF’s portfolio at that same overvaluation. Indeed, OTF is managed within the same Blue Owl credit platform, co-invests with other Blue Owl-related entities and, as OTF itself discloses, there “could be significant overlap” between OTF’s investment portfolio and the portfolios of other Blue Owl Credit Clients and other Blue Owl clients that avail themselves of Blue Owl’s exemptive co-investment order.

6. OTF’s overconcentration in software and technology investments contributes to the overvaluation of the Company’s portfolio. On April 2, 2026, Morgan Stanley analysts reported that they expect loans to companies in the software sector to result in above-average defaults of 8% in private credit loans and 5.5% annual defaults in broadly syndicated loans between the second half of 2026 through the first half of 2027 that will result in subpar returns and sluggish assets under management (“AUM”) growth.4 Assigning accurate values to debt investments in software companies is challenging due to high AI-driven disruption risks, a large “maturity wall” of debt, and a high concentration of SaaS companies in private credit with opaque, non-public pricing. As of early-2026, roughly $46.9 billion in US tech company loans are considered distressed, with a record $25 billion of software-sector loans trading below 80 cents on the dollar, according to

| 2 | See Sujeet Indap and Antoine Gera, Investment fund questions valuations in Blue Owl’s private credit portfolio, FINANCIAL TIMES (Mar. 12, 2026), available at https://www.ft.com/content/d0014b3a-94bf-4f78-8f47-64fca522e373?syn-25a6b1a6=1. |

| 3 | See Blue Owl, Q2’25 Fixed Income Investor Update, (Aug. 2025), available at https://www.blueowl.com/sites/default/files/2025-08/Blue_Owl_BDCs_Fixed_Income_Investor_Materials_2Q25.pdf |

| 4 | See David Hollerith, Blue Owl shares fall as private debt manager caps major withdrawal requests, YAHOO FINANCE (Apr. 2, 2026), available at https://finance.yahoo.com/news/blue-owl-shares-fall-as-private-debt-manager-caps-major-withdrawal-requests-150008023.html. |

3

| Provided by CourtAlert | www.CourtAlert.com |

Morningstar LSTA data.5 OTF is the largest software-focused BDC by total assets, with over $14 billion in total assets at fair value and investments in over 199 portfolio companies, on a pro forma combined basis as of December 31, 2025. With approximately 80% of its investments in software and technology, OTF is susceptible to overvaluation and market fears that AI disruption could decimate the software industry.6

7. OTF’s software exposure is an important consideration when evaluating whether Defendant’s fair value determinations on those investments are overstated. According to S&P Global, median software loan bid prices declined to 86% of par in mid-March from 92% of par in February 2026.7

8. OTF’s software exposure may also be understated by the industry classifications in its Schedule of Investments. For example, OTF classifies TK Operations Ltd. d/b/a TravelPerk as “Professional Services,” even though TravelPerk is a SaaS platform providing corporate travel booking, expense management and policy-compliance software. OTF similarly classifies Hg Saturn Luchaco Limited / LucaNet as “Diversified Financial Services,” even though LucaNet provides corporate performance management software for financial consolidation, close, planning and disclosure management. These classifications matter because they can obscure the true extent of OTF’s technology and software exposure, which is central to evaluating fair value marks, AI- related disruption risk and the reasonableness of Defendant’s fees.

| 5 | See Jason Lemkin, SaaS Markets Have Crashed in 2026. But Is Private Credit the Even Bigger Risk?, SAASTR (Feb. 20, 2026), available at https://www.saastr.com/saas-markets-have-crashed-in-2026-but-is-private-credit-the-even-bigger-risk/. |

| 6 | See Allison Morrow, More investors flee Blue Owl funds as private credit fears deepen, CNN (Apr. 2, 2026), available at https://www.cnn.com/2026/04/02/business/blue-owl-private-credit-nightcap; Jack Pitcher and Matt Wirz, Private Credit’s Exposure to Ailing Software Industry is Bigger Than Advertised, THE WALL STREET JOURNAL (Mar. 29, 2026), available at https://www.wsj.com/finance/investing/private-credits-exposure-to-ailing-software-industry-is-bigger-than-advertised-d80da378. |

| 7 | See Luri Struta, Software debt sell-off signals cyclical turn

for private equity and credit, S&P GLOBAL (Mar. 24, 2026), available at

https://www.spglobal.com/market-intelligence/en/news-insights/articles/2026/3/software-debt-sell-off-signals-cyclical-turn- |

4

| Provided by CourtAlert | www.CourtAlert.com |

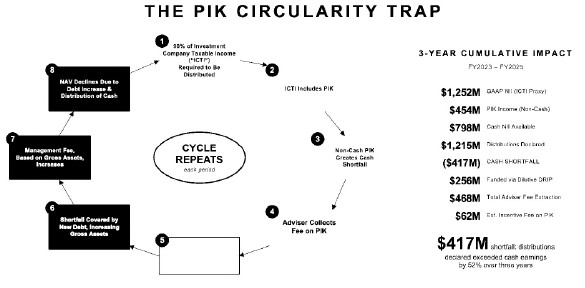

9. In addition, a significant portion of OTF’s net investment income (“NII”) consists of non-cash payment-in-kind (“PIK”) income. In a PIK financing, a borrower pays interest by adding the interest to the loan’s principal balance rather than paying cash. PIK therefore allows borrowers—often companies facing distress or cash constraints—to defer cash interest until loan maturity, causing the debt balance to grow. When OTF holds debt instruments that accrue PIK interest, it records income without receiving cash, and OTF has to pay fees to Defendant in cash based on both the payment of the PIK interest and the increase in the loan’s principal balance.

10. As a BDC that has elected to be treated as a regulated investment company for U.S. federal income tax purposes, OTF must distribute 90% of its taxable income to stockholders, and PIK interest is taxable even though it does not generate cash. OTF therefore must fund cash dividends on income it has not received in cash. In the first quarter of 2026, PIK interest and dividends accrued by OTF totaled $43 million, equal to approximately 25%, of OTF’s NII, and cash net investment income did not cover the dividend. That certain PIK terms may have been structured at origination does not eliminate the fee conflict because the economic effect is the same: OTF books non-cash income before receiving cash, Defendant earns current incentive fees on that accrued income and stockholders retain the risk that the borrower will never generate sufficient cash to repay the compounded obligation. Nor does the “structured at origination” label answer whether later amendments, waivers, refinancings or restructurings created, preserved or extended PIK treatment for credits whose ability to pay cash interest had deteriorated. Defendant’s income-based incentive fees are calculated and paid quarterly on accrued PIK income when booked, regardless of whether that income is later collected in cash. A later “collection” also does

5

| Provided by CourtAlert | www.CourtAlert.com |

not necessarily eliminate the conflict because PIK may be treated as collected through refinancing, restructuring, repayment or replacement debt, even where the borrower has not generated cash sufficient to service the original obligation. And the investment advisory agreement between Defendant and OTF (the “Advisory Agreement”) contains no true clawback requiring Defendant to return incentive fees earned on accrued PIK income that ultimately proves uncollectible. This level of PIK further supports that Defendant’s incentive fees—calculated using NII that includes accrued PIK income—are being earned on income OTF may never collect and that may not reflect true economic returns. Thus, while Defendant gets paid currently, in cash, on reported asset values and accrued income increased through PIK, OTF and its stockholders bear the downstream risk that those marks would later be reduced, that PIK income would not be collected in cash.

11. Defendant received the highest advisory compensation in OTF’s history during the same period that the portfolio was being stress-tested by software-sector repricing, macro uncertainty, rising leverage, increased PIK income and widening discounts to reported NAV. While the aggregate amount of management and income-based incentive fees paid to Defendant by OTF has increased by 191% over the last five years, from $95 million in 2021 to $276 million in 2025, the increased fees were not accompanied by a proportionate increase in the services it provided to OTF or the cost of providing investment management services to OTF.

12. Thus, as credit risk migrated from theory to reality, Defendant ensured its economics moved in the opposite direction from OTF’s stockholders. Defendant captured current cash compensation from marks and PIK income, while stockholders bore the delayed economic cost through NAV erosion, market discount, non-cash dividend coverage risk, realized and unrealized losses, and eventual non-accruals.

6

| Provided by CourtAlert | www.CourtAlert.com |

13. Plaintiffs bring this action to (i) recover for OTF the excessive and unlawful investment advisory fees extracted by Defendant in violation of its fiduciary duty under Section 36(b).

JURISDICTION AND VENUE

14. This action is brought by Plaintiffs on behalf of OTF pursuant to Section 36(b) of the ICA, 15 U.S.C. §§ 80a-35(b).

15. The Court has subject matter jurisdiction over these claims pursuant to Sections 36(b)(5) and 44 of the ICA, 15 U.S.C. §§ 80a-35(b)(5), 80(a)-44, and 28 U.S.C. § 1331.

16. Personal jurisdiction and venue are proper in this judicial district pursuant to Section 44 of the ICA, 15 U.S.C. § 80a-43, and 28 U.S.C. § 1391(b), because Defendant and OTF are headquartered in this district, transact business in this district, and many of the acts and transactions giving rise to the Plaintiffs’ claims occurred in this district.

17. No pre-suit demand on OTF’s board of directors (the “Board”) is required, as the requirements of Fed. R. Civ. P. 23.1 do not apply to actions brought under Section 36(b) of the ICA. See Daily Income Fund, Inc. v. Fox, 464 U.S. 523, 542 (1984).

THE PARTIES

| A. | Plaintiffs |

18. Plaintiff Martin Siegel is a stockholder of OTF and has continuously owned shares of OTF since at least December 29, 2025.

19. Plaintiff Thomas Kelly is a stockholder of OTF and has continuously owned shares of OTF since at least June 13, 2025.

7

| Provided by CourtAlert | www.CourtAlert.com |

| B. | Defendant |

20. Defendant is a Delaware limited liability company registered with the SEC as an investment adviser under the Investment Advisers Act of 1940. Defendant is registered as a limited liability company authorized in the State of New York and has offices at 399 Park Avenue, 37th Floor, New York, NY 10022. Defendant is a wholly owned subsidiary of Blue Owl and part of the Blue Owl Credit Platform—a direct lending platform with approximately $157.8 billion of assets under management as of December 31, 2025. Defendant focuses on direct lending to middle market companies primarily in the United States across four investment strategies, including diversified lending, technology lending, first lien lending and opportunistic lending.

| C. | Non-Party Blue Owl |

21. Blue Owl is a publicly traded alternative investment asset management company headquartered at 399 Park Avenue, 37th Floor, New York, NY 10022. Blue Owl common stock is listed on the New York Stock Exchange under the symbol “OWL.” As of December 31, 2025, Blue Owl had $307.4 billion AUM.

22. Blue Owl sponsors and controls multiple public and private BDCs in addition to OTF. Each BDC holds predominantly illiquid private credit assets and pays advisory fees to one of Blue Owl’s affiliated advisers, including Defendant. Each BDC maintains its own board of directors and audit committee, which are responsible for overseeing the adviser’s fees, valuation process, fair value determination and related governance function. The Board’s oversight does not eliminate the conflict. Defendant is the valuation designee that determines fair value for OTF’s illiquid assets, while the same directors charged with overseeing that process also serve on the boards of multiple other Blue Owl BDCs. That overlapping governance structure matters because a markdown in OTF would not be an isolated event; it could raise the same valuation questions across other Blue Owl vehicles holding similar or overlapping assets.

8

| Provided by CourtAlert | www.CourtAlert.com |

23. Blue Owl has three major product platforms: (i) Credit, which includes direct lending, alternative credit, investment grade credit and liquid credit; (ii) Real Assets, which includes primarily net lease, real estate and digital infrastructure investment strategies; and (iii) GP Strategic Capital, which primarily focuses on acquiring equity stakes in, and providing debt financing to, large private equity and private credit firms.

24. Blue Owl offers a number of products, including private funds, “Regulated Products” and Real Asset products. Blue Owl’s Regulated Products include BDCs that it manages, including OTF, OBDC, Blue Owl Capital Corporation II (“OBDC II”), Blue Owl Credit Income Corp. (“OCIC”), and Blue Owl Technology Income Corp. (“OTIC”).

| D. | Non-Party OTF |

25. OTF is a Maryland corporation headquartered at 399 Park Avenue, 37th Floor, New York, NY 10022. OTF was formed in 2018, merged with affiliated-fund Blue Owl Technology Finance Corp. II (“OTF II”) in March 2025, and its common stock began trading on the NYSE on June 12, 2025 under the symbol “OTF.” Although OTF is a publicly traded corporation, it has elected to be regulated as a BDC under the ICA.

THE ICA’S STATUTORY AUTHORITY AND FRAMEWORK

26. An investment fund pools capital from investors in order to pursue a common investment strategy. Investment funds are managed by professional asset managers who are paid a fee, plus expenses, by investors. Before the ICA, this separation of the ownership of the investment funds from the control over the funds led to substantial conflicts of interest. In an effort to mitigate conflicts of interest and protect the public from abuses in the investment fund industry, the ICA was enacted along with the Investment Advisers Act of 1940.

27. The ICA regulates the structure and operations of investment funds. The ICA seeks to protect the public primarily by requiring full disclosure of financial conditions and investment policies, and restricts risky practices like excessive leverage. The ICA details rules and regulations that investment companies must follow when offering and maintaining investment product securities, and imposes registration requirements, mandatory disclosure requirements, balance sheet constraints and fund governance rules.

9

| Provided by CourtAlert | www.CourtAlert.com |

28. With respect to governance, the ICA requires that at least 40% of the investment company’s directors be unaffiliated with its adviser, sponsor or other key affiliates. The ICA also limits transaction between funds and affiliated parties, and imposes fiduciary duties on officers, directors and investment advisers.

29. Section 36(b), 15 U.S.C. § 80(a)-35(b), was added to the ICA in 1970 after the SEC determined in the 1960s that investment advisers were still charging investment funds excessive fees that were “substantially higher” than rates they charged other clients.8

30. Section 36(b) imposes a fiduciary duty on mutual fund investment managers (and their affiliates) with respect to the receipt of compensation for services, specifically providing that:

[T]he investment adviser of a registered investment company shall be deemed to have a fiduciary duty with respect to the receipt of compensation for services, or of payments of a material nature, paid by such registered investment company or by the security holders thereof, to such investment adviser or any affiliated person of such investment adviser. An action may be brought under this subsection by the Commission, or by a security holder of such registered investment company on behalf of such company, against such investment adviser, or any affiliated person of such investment adviser … who has a fiduciary duty concerning such compensation or payments, for breach of fiduciary duty in respect of such compensation or payments paid by such registered investment company or by the security holders thereof to such investment adviser or person.

31. Under the ICA, “scrutiny of investment adviser compensation by a fully informed mutual fund board … and shareholder suits under § 36(b) are mutually reinforcing but independent mechanisms for controlling adviser conflicts of interest.”9

| 8 | See A Study of Mutual Funds Prepared for the Securities and Exchange Commission by the Wharton School of Finance and Commerce, H.R. Rep. No. 2274, p. 296 (1962). |

| 9 | Jones v. Harris Assocs. L.P., 559 U.S. 335, 336 (2010) (citations omitted). |

10

| Provided by CourtAlert | www.CourtAlert.com |

32. The test for determining whether fee compensation paid to an investment adviser is excessive is “essentially whether the fee schedule represents a charge within the range of what would have been negotiated at arm’s length in the light of all of the surrounding circumstances.”10

33. If an adviser charges a fee that is “so disproportionately large that it bears no reasonable relationship to the services rendered and could not have been the product of arm’s length bargaining,” the adviser has violated Section 36(b).11

34. To make this determination, courts consider the following non-exclusive factors set forth in Gartenberg v. Merrill Lynch Asset Management, Inc., 694 F.2d 923, 930 (2d Cir. 1981):

| (1) | the nature and quality of services being paid for by the fund and its investors; |

| (2) | whether the trustees exercised a sufficient level of care and conscientiousness in approving the investment advisory or management agreements; |

| (3) | what fees other mutual fund complexes or funds within the same fund family charge for similar services to similar mutual funds; |

| (4) | whether savings from economies of scale were passed to the funds and their investors or kept by the investment adviser; and |

| (5) | the costs of providing investment management services and the profitability of providing those services to the funds. |

35. There is no requirement to make a conclusive showing as to each Gartenberg factor and the factors are non-exclusive. The court should consider “all relevant circumstances” where other factors merit consideration when considering whether the fees charged by an adviser violated Section 36(b).12

| 10 | Gartenberg v. Merrill Lynch Asset Management, Inc., 694 F.2d 923, 928 (2d Cir. 1982). |

| 11 | Jones, 559 U.S. at 344 (citing Gartenberg, 694 F.2d at 929). |

| 12 | Jones, 559 U.S. at 347. |

11

| Provided by CourtAlert | www.CourtAlert.com |

OTF’S ORGANIZATION AND OPERATIONS

| A. | Background of OTF |

36. OTF is an externally managed, closed-end management investment company that has elected to be regulated as a BDC under the ICA.

37. “BDCs were established by Congress in 1980 as part of the Small Business Development Act, which primarily sought to encourage the flow of capital to small and middle market companies … at a time when bank balance sheets were strained.13 BDCs typically serve as a vehicle for investors to participate in direct lending to middle market companies.”14 The vast majority of BDCs were created in the last 15 years as the direct lending market scaled and matured.

38. BDCs earn money primarily through the interest payments they receive for the capital they lend.15 They also collect income from origination and prepayment fees and other lending-related charges.16 In some instances, BDCs take equity stakes in their portfolio companies and can realize capital gains. As of March 2025, BDC assets under management exceeded $475 billion.17

39. OTF has also elected to be treated as a regulated investment company (“RIC”) for U.S. Federal income tax purposes. RICs can pass income through to investors, avoiding double taxation where both the RIC and the investors pay tax on the same income. The pass-through income allowable by RICs means OTF avoids paying corporate income taxes on profits passed on to its stockholders. The only imposed income tax is on individual stockholders.

| 13 | The Basics of BDCs, HPS INVESTMENT PARTNERS (Nov. 24, 2025), available at https://d1io3yog0oux5.cloudfront.net/_0299df454c749dd6f731c180d3637cab/hlend/db/2175/46305/file/HPS+Basics+of+BDCs.pdf. |

| 14 | Id. |

| 15 | See Jonathan Kandell, Its Not Business as Usual for BDCs, INSTITUTIONAL INVESTOR (July 23, 2025), available at https://www.institutionalinvestor.com/article/its-not-business-usual-bdcs. |

| 16 | Id. |

| 17 | The Basics of BDCs, HPS INVESTMENT PARTNERS (Nov. 24, 2025), available at https://d1io3yog0oux5.cloudfront.net/_0299df454c749dd6f731c180d3637cab/hlend/db/2175/46305/file/ HPS+Basics+of+BDCs.pdf. |

12

| Provided by CourtAlert | www.CourtAlert.com |

40. Investment companies must meet certain obligations and criteria in order to qualify as a RIC. A RIC must earn at least 90% of its income from capital gains, interest, or dividends from investments. It must also distribute a minimum of 90% of its net investment income in the form of interest, dividends, or capital gains to its stockholders. Additionally, at least 50% of RIC’s assets must be in cash, cash equivalents, or securities.

41. OTF’s investment strategy focuses on primarily originating and making loans to, and making debt and equity investments in, technology-related, specifically software, middle-market companies based primarily in the United States. OTF states that it intends to invest at least 80% of the value of its total assets in “technology-related” companies and that, within enterprise software, it focuses on application software, systems and infrastructure software and fintech and payments software.

42. OTF’s portfolio investments consist primarily of first lien debt instruments, but also includes substantial investments in second-lien secured debt, unsecured debt, special financing debt investments, joint ventures, and common and preferred equity investments. OTF invests in companies in various industries, with its largest investments in software and technology sector, accounting for approximately 70% of total assets.

43. As of March 31, 2026, OTF had investments in 203 portfolio companies, with an aggregate fair value of $14.1 billion.

44. OTF also invests in Blue Owl-related specialty financing portfolio companies, including Fifth Season Investments LLC, LSI Financing 1 DAC, LSI Financing LKLC, AAM Series 1.1 Rail and Domestic Intermodal Feeder, LLC and AAM Series 2.1 Aviation Feeder, LLC, and Blue Owl Cross-Strategy Opportunities LLC.

13

| Provided by CourtAlert | www.CourtAlert.com |

45. OTF also invests in Blue Owl-related joint ventures, Blue Owl Credit SLF LLC (“Credit SLF”), Stripe Blue Owl Holdings LLC (“Stripe Blue Owl”) and Blue Owl Leasing LLC (“Blue Owl Leasing”).

46. Credit SLF, Blue Owl Leasing, and Stripe Blue Owl Holdings are disclosed as controlled affiliated investments, and the remaining investment vehicles are disclosed as non-controlled affiliated investments. OTF’s public filings provide no look-through to underlying assets in those investment vehicles, and OTF does not consolidate its interest in those investment vehicles.

47. Both the joint ventures and the specialty finance portfolio companies use OTF’s capital to support acquisitions. OTF’s affiliated and controlled investments add an additional layer of opacity because stockholders do not receive the same borrower-level look-through disclosure for the assets held by these vehicles. That opacity is significant because Defendant’s fees are based on OTF’s reported assets and income, including assets held through affiliated and controlled vehicles.

48. OTF is overseen by a Board consisting of six directors, five of whom are claimed to be “independent” directors. The Board has established a Nominating and Corporate Governance Committee, a Compensation Committee, an Audit Committee, and a Co-Investment Committee. The Chairman of the Board, currently Edward D’Alelio, acts as a liaison with Defendant.

49. Like many other investment funds, OTF does not have employees or facilities of its own. OTF’s operations are conducted by related-party service providers pursuant to contracts with Defendant.

14

| Provided by CourtAlert | www.CourtAlert.com |

50. The Board is responsible for selecting and monitoring OTF’s service providers, including its investment adviser, and approving all agreements with service providers, among other things.

51. The same directors on the OTF Board oversee five other Blue Owl BDCs. OTF’s five purportedly independent directors—Edward D’Alelio, Christopher M. Temple, Eric Kaye, Melissa Weiler and Victor Woolridge—oversee five companies in the Blue Owl “Fund Complex,” including OTF, OBDC, OBDC II, OCIC, and OTIC and received substantial compensation in 2025. Thus, the same directors charged with overseeing Defendant’s fees, valuation process, and conflicts at OTF also had recurring, highly compensated positions across the Blue Owl Fund Complex. That structure gave the Board further reason to avoid challenging fee and valuation practices that were not unique to OTF, including Defendant’s role as valuation designee, its control over marks on Level 3 assets that are not publicly traded or whose market prices are not readily available, the absence of meaningful breakpoints, and the lack of a true clawback for incentive fees earned on accrued PIK income.

| Director |

Other Blue Owl BDC boards disclosed by OTF |

2025 compensation from OTF |

2025 total compensation from Blue Owl Fund Complex |

|||||||

| Edward D’Alelio |

OBDC, OBDC II, | $ | 290,000 | $ | 1,442,806 | |||||

| OCIC, OTIC | ||||||||||

| Christopher M. Temple |

OBDC, OBDC II, | $ | 285,000 | $ | 1,416,500 | |||||

| OCIC, OTIC | ||||||||||

| Eric Kaye |

OBDC, OBDC II, | $ | 280,000 | $ | 1,390,194 | |||||

| OCIC, OTIC | ||||||||||

| Melissa Weiler |

OBDC, OBDC II, | $ | 275,000 | $ | 1,363,889 | |||||

| OCIC, OTIC | ||||||||||

| Victor Woolridge |

OBDC, OBDC II, | $ | 275,000 | $ | 1,363,889 | |||||

| OCIC, OTIC | ||||||||||

15

| Provided by CourtAlert | www.CourtAlert.com |

| B. | OTF’s Recent Performance |

52. On March 24, 2025, OTF merged with OTF II in a related party transaction, with OTF as the surviving company, making OTF the largest software-focused BDC by total assets with over $12 billion of total assets at fair value and investments in 180 portfolio companies, on a pro forma combined basis as of December 31, 2024. Prior to the merger, OTF had investments in 148 portfolio companies with an aggregate fair value of $6.4 billion.

53. On November 4, 2025, OTF announced that the Board approved a $200 million stock repurchase program, for which purchases may be made at management’s discretion from time to time in open market transactions. As of December 31, 2025, OTF repurchased approximately $64.6 million of OTF common stock at 82% of price-to-book value, accretive to NAV per share in the fourth quarter of 2025.

54. On May 6, 2026, OTF issued its financial results for its the quarter ended March 31, 2026. Those results reflected weakening performance: OTF reported core earnings per share of $0.29, down from $0.41 per share over the prior year and missing expectations. OTF also reported revenue of $325.94 million, below the consensus estimate of $341.0 million. OTF further reported adjusted NII of $0.29 per share, below the consensus estimate of $0.31 per share and the lowest level of adjusted net NII that OTF reported over the last 12-month period. OTF’s NAV per share fell 4.8% to $16.49 per share. Several additional performance indicators deteriorated in the first quarter of 2026, including: (i) weighted-average LTV rose to about 40%, up from 34% in the prior quarter; (ii) OTF reported net realized and change in unrealized losses of $391.2 million, which were the largest losses suffered within OTF’s portfolio since inception; and (iii) total expenses rose to $153 million, which is nearly double the total expenses from the prior year, largely driven by OTF’s increase in total debt.

16

| Provided by CourtAlert | www.CourtAlert.com |

55. Management said market volatility around software and technology assets weighed on valuations even as underlying credit performance remained strong, and that more than 80% of the quarter’s write-down was attributable to mark-to-market movements tied to wider technology credit spreads.18 As of early-March 2026, OTF common stock has traded at a 32% discount to NAV.

56. In connection with the first quarter 2026 results, OTF declared a $0.31 per share dividend plus an additional five cent per share dividend, matching the previous quarter. In addition, having already repurchased approximately $64.6 million of OTF common stock during the fourth quarter 2025, OTF also announced on February 18, 2026 that the Board approved a new repurchase program of up to $300 million of OTF’s common stock, replacing the prior $200 million authorization. OTF’s stock repurchases in the fourth quarter 2025 at an 18% discount of price-to-book value were a strategic effort by OTF to prop up its NAV, as the stock was trading at a more than 20% discount to NAV per share since at least November 2025.

57. Since its inception, OTF’s share price has declined by more than 33.8%. Even when including all distributions paid out to stockholders, the total return still sits at a loss of more than 26% over the same time frame.19 And as of May 12, 2026, OTF is among the most deeply discounted BDCs, as it trades at price/NAV of 0.66x, while the sector average price/NAV is 0.81x.20

| 18 | See Blue Owl Technology Finance Q1 Earnings Call Highlights, MARKETBEAT (May 14, 2026), available at https://finance.yahoo.com/markets/stocks/articles/blue-owl-technology-finance-q1-071238464.html. |

| 19 | See Cain Lee, Blue Owl Technology Finance: I See The Potential In This BDC, But It’s Not A Buy Yet, SEEKING ALPHA (May 20, 2026), available at https://seekingalpha.com/article/4907215-blue-owl-technology-finance-i-see-the-potential-in-this-bdc-but-not-a-buy-yet. |

| 20 | See Roberts Berzins, OTF: The Biggest BDC Bargain, SEEKING ALPHA (May 12, 2026), available at https://seekingalpha.com/article/4903003-otf-biggest-bdc-bargain. |

17

| Provided by CourtAlert | www.CourtAlert.com |

58. The private credit sector has come under increased scrutiny as AI-related disruption, fund outflows, and credit-stress concerns have pressured alternative asset managers’ stocks. Much of that pressure has been tied to software-sector repricing, as AI-driven disruption has raised concerns about software borrowers’ valuations and credit quality. Shortly after OTF began trading on the NYSE on June 12, 2025 (the “Listing Date”), investors in Blue Owl’s affiliated private BDCs submitted unprecedented redemption requests.21 Investor withdrawals were originally linked to valuation, as investors worried Blue Owl’s loans were not worth what it said, partly because of the BDCs’ lending was to software companies, and the publicly traded BDCs with nearly identical portfolios were trading at a big discount to NAV.22 Those requests were also driven by concerns about private-credit risk, market volatility, and potential AI-driven disruption at portfolio companies.23 Blue Owl’s private fund (OBDC II) saw surges in withdrawal requests above the fund’s preset 5% per quarter limit, and by late-February 2026, Blue Owl announced it was permanently halting redemptions from OBDC II and began liquidating certain assets to raise cash.24 By April 2, 2026, two additional Blue Owl private credit vehicles—OCIC and OTIC—were facing $5.4 billion in redemption requests, and Blue Owl announced that each fund was limiting outflows to 5% of its value.25 Publicly traded Blue Owl itself has lost 40% of its market value this year alone.

| 21 | Blue Owl is spoiling private credit’s sales pitch, FINANCIAL TIMES (Feb. 23, 2026), available at

|

| 22 | Blue Owl is spoiling private credit’s sales pitch, FINANCIAL TIMES (Feb. 23, 2026), available at

|

| 23 | See Maureen Farrell, New Limits on Investors and a Debt Downgrade Add to Private Credit Woes, NEW YORK TIMES (Mar. 24, 2026), available at https://www.nytimes.com/2026/03/24/business/moodys-private-credit-downgrade.html; Alex Nicoll, Ares is the latest private credit player to limit withdrawals after investors ask to redeem their money, BUSINESS INSIDER (Mar. 24, 2026), available at https://www.businessinsider.com/ares-limits-private-credit-fund-withdrawals-2026-3. |

| 24 | See Black and Blue Owl, FINANCIAL TIMES (Feb. 26, 2026), available at https://www.ft.com/content/4f57094c-6255-431b-a711-8112e49725bb. |

| 25 | See Alex Nicoll, Blue Owl is facing $5.4 billion in redemption requests. Here are 6 things to know about the private credit firm, BUSINESS INSIDER (Apr. 2, 2026), available at https://www.businessinsider.com/blue-owl-private-credit-firm-redemptions-2026-4. |

18

| Provided by CourtAlert | www.CourtAlert.com |

DEFENDANT IS OTF’S INVESTMENT ADVISER,

ADMINISTRATOR, AND VALUATION DESIGNEE

59. Defendant serves as the investment adviser to, and manages the day-to-day operations of, OTF pursuant to the terms of the Advisory Agreement. Defendant’s services under the Advisory Agreement are not exclusive, and Defendant is free to (and does) provide similar advisory services to other entities, including Blue-Owl-affiliated funds.

60. Defendant is responsible for managing OTF’s portfolio of securities, including determining the composition of OTF’s portfolio and the nature and timing of any changes to the portfolio, structuring investments, determining the investments that OTF makes, retains or sells, and determining the fair value of debt and equity securities that are not publicly traded and whose market prices are not readily available.

61. Defendant is also the valuation designee (the “Valuation Designee”) of OTF’s portfolio investments pursuant to SEC Rule 2a-5 under the ICA, 17 C.F.R. § 270.2a-5.

62. SEC Rule 2a-5 establishes a framework for how BDCs determine the fair value of their investments. It requires investment companies to assess valuation risks and set fair value methodologies, and it allows boards to designate the investment adviser for valuation, subject to board oversight.

63. OTF’s Board is charged with overseeing Defendant’s valuation process. As part of its oversight function, the Audit Committee is to report to the Board on any valuation matters requiring the Board’s attention. Under Rule 2a-5, the Board reins ultimate responsibility for fair valuation determinations.

19

| Provided by CourtAlert | www.CourtAlert.com |

64. OTF’s portfolio comprises so called “Level 3 assets,” meaning debt and equity securities that are not publicly traded or whose market prices are not readily available, so the fair value of those assets come from models controlled by Defendant.

65. OTF values its investments quarterly at fair value as determined by Defendant, based on, among other things, input of the Board’s Audit Committee and any third-party valuation firm(s) engaged at the direction of Defendant.

66. As the Valuation Designee, Defendant provides the Audit Committee a summary description of material fair value matters that occurred in the prior quarter and written assessment of the adequacy and effectiveness of its fair value process.

67. The determination of fair value of the portfolio investments is subjective, in part, and Defendant has a conflict of interest in determining fair value. Specifically, Defendant determines the fair value of illiquid private credit instruments—assets lacking observable market quotations—using internal models, discounted cash flow assumptions, sponsor projections and other Level 3 inputs. Defendant’s compensation is then calculated by reference to metrics affected by those determinations: the management fee is based on average gross assets, including assets purchased with borrowed amounts, and the income-based incentive fee is calculated on pre-incentive fee net investment income, which includes accrued income even when not received in cash. As a result: (i) higher valuations on OTF’s portfolio assets increase advisory fees; (ii) those fees are paid out of OTF’s assets; and (iii) economically, OTF’s stockholders bear the cost dollar-for-dollar through reduced equity.

20

| Provided by CourtAlert | www.CourtAlert.com |

68. In other words, Defendant is the same affiliated entity that determines fair value for illiquid portfolio assets and receives compensation tied to the resulting gross-asset base and accrued-income base. This structure creates an inherent incentive for Defendant to inflate, stabilize, or delay markdowns of portfolio valuations, particularly during periods of credit spread widening, software-sector repricing, liquidity stress or elevated PIK accruals.

69. Defendant serves the additional role as OTF’s Administrator pursuant to an administration agreement between Defendant and OTF (the “Administration Agreement”). Pursuant to the terms of the Administration Agreement, Defendant performs, or oversees, required administrative services, which includes providing office space, equipment and office services, maintaining financial records, preparing reports to stockholders and reports filed with the SEC, and managing the payment of expenses and the performance of administrative and professional services rendered by others, which could include employees of the Defendant or its affiliates. OTF reimburses Defendant for services performed under the Administration Agreement.

THE ADVISORY COMPENSATION STRUCTURE

70. All investment professionals are provided by and paid for by Defendant, and OTF pays its allocable portion of the compensation paid by Defendant to OTF’s Chief Compliance Officer and Chief Financial Officer and their respective staffs based on a percentage of time those individuals devote to OTF, which is estimated.

71. OTF bears all other costs and expenses of its operations, administration and transactions, including (i) investment advisory fees, including management fees and incentive fees, to Defendant pursuant to the Advisory Agreement and the Administration Agreement; (ii) its allocable portion of overhead and other expenses incurred by Defendant in performing its administrative obligations under the Administration Agreement; and (iii) all other costs and expenses of its operations and transactions.

21

| Provided by CourtAlert | www.CourtAlert.com |

72. The fees OTF pays Defendant for its advisory services are governed by the Advisory Agreement.

73. The Advisory Agreement is to be approved annually by a majority of the OTF Board or by holders of a majority of OTF’s outstanding voting securities, as well as a majority of the independent directors. The current Advisory Agreement became effective on May 18, 2021. On May 5, 2025, the Board approved the continuation of the Advisory Agreement and concluded that the advisory fee rates were reasonable in relation to the services provided.

74. Pursuant to the Advisory Agreement, OTF pays Defendant fees for its investment advisory services consisting of two components: a management fee and an incentive fee.

75. Defendant’s management fee and incentive fees increased after the Listing Date, which the existing Advisory Agreement provided for and which the Board approved.

| A. | Management Fee |

76. Defendant’s base management fee is payable quarterly in arrears at an annual rate of (i) 1.50% of OTF’s average gross assets, excluding cash and cash equivalents but including assets purchased with borrowed amounts, that are above an asset coverage ratio of 200% calculated under Sections 18 and 61 of the ICA, and (ii) 1.00% of OTF’s average gross assets, excluding cash and cash equivalents but including assets purchased with borrowed amounts, that are below an asset coverage ratio of 200%. For purposes of the Advisory Agreement, gross assets means OTF’s total assets determined on a consolidated basis in accordance with GAAP, excluding cash and cash equivalents, but including assets purchased with borrowed amounts.

22

| Provided by CourtAlert | www.CourtAlert.com |

77. Prior to the June 12, 2025 Listing Date, Defendant’s base management fee was payable at an annual rate of 0.90% of OTF’s average gross assets, excluding cash and cash equivalents but including assets purchased with borrowed amounts, plus the average of any remaining unfunded capital commitments; provided that no management fee was charged on gross assets below an asset coverage ratio of 200% calculated under Sections 18 and 61 of the ICA.

| B. | Incentive Fee |

78. OTF pays Defendant an incentive fee with two separate components: an income- based incentive fee and a capital gains incentive fee.

79. The income-based incentive fee is calculated and paid quarterly in arrears. The fee equals 100% of pre-incentive fee net investment income in excess of a 1.5% quarterly hurdle until Defendant has received 17.5% of total pre-incentive fee net investment income for that quarter, and 17.5% of all remaining pre-incentive fee net investment income above 1.82% quarterly. The 100% catch-up is designed to provide Defendant with 17.5% of all pre-incentive fee net investment income once the catch-up is achieved.

80. Prior to the Listing Date, Defendant’s income incentive fee was lower and equaled 100% of the pre-incentive fee net investment income after OTF cleared a 1.5% quarterly hurdle, until Defendant received 10% of the total pre-incentive fee net investment income. And for pre-incentive fee net investment income in excess of 1.67%, Defendant was paid 10% of all remaining pre-incentive fee net investment income.

81. Pre-incentive fee net investment income includes dividends, interest and fee income accrued during the quarter, minus operating expenses. Pre-incentive fee net investment income includes accrued income that OTF may not have received in cash, including original issue discount, PIK interest and zero-coupon securities, and Defendant is not obligated to return incentive fees it receives on PIK interest that is later determined to be uncollectible in cash by OTF.

23

| Provided by CourtAlert | www.CourtAlert.com |

82. That feature creates a risk of future nonpayment, even as OTF issues quarterly payments to Defendant as if it had been paid in cash. When a borrower pays PIK interest, OTF records income even though cash collection depends on future repayment or refinancing. If the borrower defaults or cannot refinance at maturity, OTF may never collect the cash corresponding to that accrued income. Defendant nevertheless receives quarterly cash incentive fees on accrued PIK income when earned, and the Advisory Agreement does not require Defendant to return those fees if the accrued income later proves uncollectible. Thus, PIK income allows Defendant to collect cash fees on non-cash, contingent income while OTF and its stockholders retain the collection risk.

83. The second component—the capital gains incentive fee—is payable annually in arrears and equals 17.5% of cumulative realized capital gains from September 30, 2025 (the quarter-end date following the Listing Date of June 12, 2025), net of cumulative realized capital losses and unrealized capital depreciation.

| C. | The Magnitude of Advisory Fees Paid by OTF |

84. To the extent Section 36(b) provides a damages limitation “start date” (but no corresponding end date), damages are limited to only those excessive fees charged during the period beginning one year prior to the complaint filing (but extending through the pendency of the action).

24

| Provided by CourtAlert | www.CourtAlert.com |

85. On February 18, 2026, OTF reported its advisory fees for the year ended December 31, 2025.26 The aggregate amount of management and incentive fees OTF paid to Defendant has increased by 191% over the last five years, from $95 million in 2021 to $276 million in 2025.

86. The table below sets forth the investment management fees and incentive fees that OTF paid to Defendant over the past five years:

| 2021 | 2022 | 2023 | 2024 | 2025 | ||||||||||||||||

| Management Fees |

$ | 47 million | $ | 56 million | $ | 59 million | $ | 57 million | $ | 145 million | ||||||||||

| Income-Based Incentive Fees |

$ | 20 million | $ | 28 million | $ | 41million | $ | 41 million | $ | 93 million | ||||||||||

| Capital Gains Incentive Fee |

$ | 28 million | ($ | 20 million | ) | $ | 0.3 million | ($ | 5 million | ) | $ | 38 million | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Fees |

$ | 95 million | $ | 64 million | $ | 100.3 million | $ | 93 million | $ | 276 million | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

87. Because Defendants’ fees increased following the Listing Date, the advisory fees OTF pays Defendant are expected to be markedly higher in 2026.

88. The scale of Defendant’s compensation is even more stark when compared to the cash value realized by OTF’s investors. In 2025, OTF reported approximately $276 million of total advisory compensation paid or accrued to Defendant. During the same period, OTF generated approximately $714 million of gross cash value for investors, measured as distributions declared, net realized gains and share repurchases. After deducting Defendant’s advisory compensation, the net cash value realized by investors was approximately $438 million. Thus, for every $1.00 of net cash value realized by OTF investors after advisory fees, Defendant received approximately $0.63 in advisory compensation.

| 26 | See Blue Owl Technology Finance Corp., Form 10-K (filed on Feb. 18, 2026), at F-58, available at https://www.sec.gov/Archives/edgar/data/1747777/000174777726000012/ortf-20251231.htm. (“2025 10-K”). |

25

| Provided by CourtAlert | www.CourtAlert.com |

DEFENDANT EXTRACTED EXCESSIVE FEES FROM OTF

| A. | Defendant’s Compensation Structure Generates Excessive Fees |

89. The Advisory Agreement includes an advisory fee structure based on OTF’s gross assets, which is problematic for several reasons.

90. First, OTF’s assets are Level 3 assets that are not publicly traded or whose market prices are not readily available. This means that the value of those assets is determined by Defendant and come from models controlled by Defendant. Defendant’s fee is based on those self-interested fair value determinations, where Defendants’ determination of higher valuations results in higher fees paid to Defendant.

91. Second, PIK interest is capitalized into the principal balance and amortized cost basis of the underlying investment. As a result, OTF records additional investment income and a higher contractual amount owed, even though it has not received corresponding cash and ultimate collection may depend on the borrower’s future ability to refinance or repay. To the extent those accrued amounts are reflected in the asset’s fair value, they also increase the total asset based on which Defendant’s management fee is calculated.

92. Third, Defendant’s incentive fee is based on a percentage of pre-incentive fee NII, which includes, in the case of investments with a deferred interest feature (such as a PIK interest), accrued income that OTF may not have received in cash. Thus, in instances where Defendant has received an incentive fee based on deferred income that is ultimately uncollected by OTF, the Advisory Agreement is drafted such that the fee structure does not provide a clawback requiring Defendant to return to OTF the incentive fees previously received on that unrealized interest income. Although future NII may be lower if the investment later stops accruing income, it is placed on non-accrual, or is written down, that future effect does not compensate OTF for cash incentive fees already paid to Defendant on a quarterly basis on income that was never actually realized.

26

| Provided by CourtAlert | www.CourtAlert.com |

93. These three features of Defendant’s compensation framework not only result in excessive advisory fees, but also fail to address inherent conflicts of interest associated with Defendant’s management services and compensation.

| 1. | Defendant Controls and Determines the Fair Value of OTF’s Portfolio Investments and Higher Valuations of those Assets Results in Higher Fees to Defendant |

94. As OTF’s Valuation Designee, Defendant’s valuation practices suffer from inherent conflicts of interest because Defendant simultaneously controls the marks on the assets and benefits financially from higher marks through management fees (amounting to $145 million in 2025) and incentive fees ($93 million), including fees on non-cash PIK income.

95. An analysis of Defendant’s valuation practices shows that Defendant maintains value marks of OTF’s portfolio assets at levels inconsistent with observable market evidence, economic conditions, and the evolving risk profile of OTF’s portfolio.

96. For the first quarter of 2026, OTF reported NAV per share of $16.49 per share, down from $17.33 in the prior quarter. Over the past year, OTF’s share price has persistently traded at a 20% or more discount to NAV, and OTF’s stock currently trades at about a 30% discount to NAV.27 Yet, Defendant has collected management fees on assets that the market has priced at lower levels, thereby resulting in excessive management fees to Defendant.

| 27 | See Brian Moriarty and Jack Shannon, Blue Owl’s Misfire Offers a Lesson in Semiliquid Fund Risks, MORNINGSTAR (Nov. 21, 2025), available at https://www.morningstar.com/alternative-investments/blue-owls-misfire-offers-lesson-semiliquid-fund-risks; Blue Owl Capital Corporation: A Questionable Discount to NAV, SEEKING ALPHA (Mar. 18, 2026), available at https://seekingalpha.com/article/4883827-blue-owl-capital-corporation-a-questionable-discount-to-nav. |

27

| Provided by CourtAlert | www.CourtAlert.com |

| 2. | Defendant Benefits from PIK Interest in OTF’s Portfolio Because it Increases the Gross Assets on Which Defendant’s Management Fee is Based |

97. As of March 31, 2026, OTF reported PIK interest and dividend income of 13.1% investment income, which is high relative to peers (with average ~9%).28 And the reported $42.5 million of PIK interest and PIK dividend income in the first quarter of 2026 make up approximately 25%, of OTF’s NII.

98. PIK interests increase OTF’s future investment income, which increases its gross assets, and as a result increases Defendant’s management fee. Yet, PIK instruments carry an increased credit risk and may become uncollectible by OTF. And even though some of the PIK interest may be uncollected by OTF, Defendant’s management fee is nevertheless calculated on OTF’s gross assets, which include PIK interest.

99. Approximately $7.4 million of Defendant’s management fee in 2025 was attributable to PIK income, which was excessive to the extent that income was uncollected by OTF.

| 28 | See Rubicon Associates, Ares Capital: Double-Digit Yield From A Gold Standard BDC, Seeking Alpha (May 5, 2026), available at https://seekingalpha.com/article/4898334-ares-capital-double-digit-yield-from-a-gold-standard-bdc; Fitch Expects to Rate Ares Capital Unsecured Notes ‘BBB,’ Fitch Ratings (May 5, 2026), available at https://www.fitchratings.com/research/corporate-finance/fitch-expects-to-rate-ares-capital-unsecured-notes-bbb-05-05-2026; Ares Capital Corporation: The Titan of Private Credit – And A 9% Dividend, Opportunitycosts.substack.com (Nov. 30, 2025), available at https://opportunitycosts.substack.com/p/ares-capital-corporation-the-titan. |

28

| Provided by CourtAlert | www.CourtAlert.com |

| 3. | Defendant Benefits from Increased Income Incentive Fees from PIK Interest Even When OTF is Harmed from Unrealized Investment Income |

100. Defendant’s income incentive fee includes a component based on 17.5% of NII above a 1.5% quarterly hurdle. PIK income flows into NII despite generating zero cash, thereby directly increasing the income-based incentive fee. At the same time, accrued PIK interest is capitalized in the value of portfolio investments and included in OTF’s gross assets, which form the basis for the management fee, thereby increasing that fee as well. In addition, by increasing reported asset values and delaying the recognition of unrealized depreciation and realized losses, PIK income increases the magnitude of capital gains incentive fees, which are calculated net of such losses and depreciation. Accordingly, a single PIK dollar benefits Defendant across all three components of its compensation.

101. Defendant’s incentive fees are also paid on income that remains contingent on the borrower’s future ability to refinance or repay the underlying obligation, and the fee structure set forth in the Advisory Agreement does not require repayment of incentive fees previously paid on income that ultimately proves uncollectible by OTF.

102. Defendant thus receives excessive incentive fees when OTF does not ultimately realize that interest income.

| B. | The Gartenberg Factors |

103. The amount of advisory fees that Defendant extracted and retained from OTF is so disproportionately large that it bears no reasonable relationship to the services rendered in exchange for that fee, and could not have been negotiated through arm’s-length bargaining, as demonstrated by applying the Gartenberg factors.

| 1. | Gartenberg Factor 1: Nature and Quality of the Services Rendered |

104. OTF primarily invests in Level 3 private credit assets that require active monitoring and valuation.

105. Defendant has maintained fair value marks for OTF’s portfolio assets at levels inconsistent with observable market evidence, economic conditions, and the changing risk profile of its portfolio—particularly its PIK securities positions.

29

| Provided by CourtAlert | www.CourtAlert.com |

106. Defendant’s improper valuation is incentivized by the inherent structural conflicts of which Defendant simultaneously controls the marks on the assets and benefits financially from higher marks through management fees and incentive fees (totaling $238 million in 2025 alone), which include fees that are based, in part, on non-cash PIK income or other deferred income that Defendant is not obligated to return even if the asset is later determined to be uncollectible by OTF.

107. The first quarter of 2026 illustrates the disconnect between Defendant’s compensation and stockholder outcomes. OTF reported net investment income after taxes of approximately $171.3 million but also reported total net realized and unrealized losses of approximately $391.2 million and a net decrease in net assets from operations of approximately $219.9 million. Nevertheless, Defendant earned approximately $28.1 million of income-based incentive fees for the quarter and approximately $53.9 million of management fees.

108. Had Defendant assigned accurate (lower) marks to OTF’s portfolio assets, that would directly reduce is advisory fees.

| 2. | Gartenberg Factor 2: Profitability to the Adviser |

109. While information concerning Defendant’s profitability in providing services to OTF is not publicly available, there are indications that Defendant’s profits are substantially higher than average, and therefore that the advisory services Defendant provides to OTF is highly profitable to Defendant.

110. Public filings of Blue Owl, Defendant’s parent company, include meaningful data on Blue Owl’s fee-related earnings (“FRE”) margins. Given that Defendant is Blue Owl’s subsidiary entity receiving fees from Blue Owl’s BDCs and operates within the same broad platform, similar economics and margins would apply to Defendant.

30

| Provided by CourtAlert | www.CourtAlert.com |

111. Blue Owl’s FRE margins were 59.4% in 2024 and 58.3% in 2025.

112. According to two 2025 studies on advisory firm profitability, registered investment advisory firms typically average profit margins ranging from 25% up to 40%.29

113. Accordingly, Defendant’s estimated profit margins of more than 58% in 2025 demonstrate that Defendant’s advisory services to OTF is excessively profitable, with a profit margin well above average. This factor demonstrates Defendant’s fees are excessive.

114. Furthermore, additional publicly available information shows that Defendant’s advisory fees are excessive. According to Defendant’s regulatory filings, as of March 31, 2026, it manages a total of five accounts, with a combined total of more than $16.1 billion AUM.30

115. OTF alone paid Defendant advisory fees totaling $238 million in 2025, based on OTF’s total reported assets of $12.4 billion. Considering that Defendant manages an additional $1.4 billion in assets for other Blue Owl-affiliated entities, and assuming a similar fee structure that Defendant has with OTF, it is estimated that Defendant receives additional advisory fees of at least $16.7 million per year, and together with fees paid by OTF, a total nearly $255 million in advisory fees in 2025.31

| 29 | See Philip Palaveev, Too Much of A Good Thing?, FINANCIAL ADVISOR (Sept. 1, 2024), available at https://www.fa-mag.com/news/too-much-of-a-good-thing-ria-profits- 79221.html#:~:text=Amazing%20Profits,Amazing%20Productivity; see also Steve Randall, Advisory firms hit record profits, but growth slips into “prosperous stagnation,” INVESTMENT NEWS (Aug. 8, 2025), available at https://www.investmentnews.com/practice-management/advisory-firms-hit-record-profits-but-growth-slips-into-prosperous-stagnation/261640. |

| 30 | See Blue Owl Technology Credit Advisors LLC, Form ADV (filed on Mar. 31, 2026), available at https://files.adviserinfo.sec.gov/IAPD/content/viewform/adv/sections/iapd_AdvIdentifyingInfoSection.as px?ORG_PK=297497&FLNG_PK=03A9E98C000801F1035F57A200749A39056C8CC0. |

| 31 | Defendant’s $238 million fee from OTF in 2025 represents 1.91% of OTF’s total assets. Considering that Defendant manages at least an additional $1.4 billion AUM for other Blue Owl investment vehicles, applying that same 1.91% of AUM fee amount paid by OTF to Defendant to $1.4 billion AUM, results in $16.7 million. |

31

| Provided by CourtAlert | www.CourtAlert.com |

116. Additionally, the advisory fee structure allows for fees that grow with leverage and pays income incentive fees in quarters where OTF recognizes a loss. As detailed herein, in the first quarter 2026, NAV per share fell 4.8% and OTF posted a decrease in net assets from operations of nearly $220 million, or $(0.47) per share. In that same quarter, Defendant increased leverage from 0.75x to 0.85x debt-to-equity, increasing debt to $7.0 billion, up from $6.3 billion. Defendant collects its management fee on OTF’s entire asset base however it is financed, increasing debt holds the fee base up even as equity value declines. Meaning, in the first quarter of 2026, Defendant earned advisory fees on net investment income of $171.3 million, or $0.37 per share, in a quarter where stockholders lost $0.47 per share on a total basis. And that income incentive fee can accrue on PIK income that never arrives in cash. In this instance, Defendants profitability is untethered from fund performance—the fee grows with leverage and OTF pays income incentive fees in loss quarters. Such fees are also indicative of the non-arm’s length fee structure approved by the Board.

117. This fee burden was also disproportionate to the cash economics realized by OTF stockholders. In 2025, Defendant received approximately $0.63 in advisory compensation for every $1.00 of net cash value realized by OTF investors after advisory fees. That ratio underscores the excessive nature of Defendant’s compensation and the asymmetry of the Advisory Agreement: Defendant captured substantial current economics while stockholders bore the downside risk of NAV decline, market discount, PIK non-collection, leverage and delayed credit-loss recognition.

118. Defendant provides advisory services exclusively to Blue Owl-affiliated entities and manages portfolios with overlapping investments, including through co-investment arrangements across affiliated funds.32 This structure allows Defendant to originate, diligence, and monitor substantially similar investments across multiple vehicles simultaneously, reducing marginal costs while generating multiple streams of fee revenue tied to the same or similar underlying assets. Moreover, as discussed above, Defendant incurs limited marginal costs as assets scale.

| 32 | See Blue Owl Capital Corporation, Form 10-K for the year ended December 31, 2025, at F-77 (filed on Feb. 18, 2026), available at https://www.sec.gov/Archives/edgar/data/1655888/000165588826000010/obdc-20251231.htm (“there could be significant overlap in the Company’s investment portfolio and the investment portfolios of the |

32

| Provided by CourtAlert | www.CourtAlert.com |

119. Accordingly, Defendant’s receipt of such substantial fee revenues, while managing overlapping Blue Owl portfolios with shared infrastructure and limited incremental costs, and in some instances even in quarters where OTF recognizes a loss, is excessive in relation to the services Defendant provides.

| 3. | Gartenberg Factor 3: Fall-Out Benefits to the Adviser |

120. Fall-out benefits are indirect economic benefits an investment adviser receives from its relationship with a fund, separate from the advisory fee itself, including affiliated fee streams, expense reimbursements, access to investment opportunities, market information, reputational benefits, and platform efficiencies. OTF’s captive relationship with Defendant gives rise to these benefits because Defendant uses OTF’s scale, portfolio, and investor capital to support Blue Owl’s broader affiliated platform in ways that would not accrue but for the captive relationship.

121. For example, as the direct result of Defendant serving as OTF’s investment adviser, Defendant was engaged to provide other services to OTF, pursuant to separate service contracts, and receives substantial fees for providing such other services. Defendant also serves as OTF’s Administrator and receives additional compensation pursuant to its Administration Agreement, for providing OTF with administrative services.

BDCs, interval fund, private funds and separately managed accounts managed by the Blue Owl Credit Advisers [] and/or other funds managed by the Adviser or its affiliates that avail themselves of the Order”).

33

| Provided by CourtAlert | www.CourtAlert.com |

122. Pursuant to the Administration Agreement, OTF paid Defendant for its administrative services as follows:

| 2023 Admin Fees | 2024 Admin Fees | 2025 Admin Fees | ||

| $7.7 million | $3.6 million | $3.0 million | ||

123. Defendant operates OTF as part of a broader Blue Owl platform managing multiple affiliated BDCs, private funds and other investment vehicles, with overlapping investment strategies and portfolios. Blue Owl originates deals centrally and allocates them across multiple affiliated vehicles (including OTF), all of which pay fees to Blue Owl. As a result, Defendant can leverage shared personnel, infrastructure, and investment sourcing capabilities across multiple vehicles, reducing its marginal costs while generating additional revenue streams tied to each affiliated fund. Because of this shared pipeline, OTF is likely not receiving differentiated investment management services commensurate with the management fees it pays to Defendant.

124. Defendant also benefits from co-investment arrangements and overlapping portfolio positions across Blue Owl-affiliated vehicles, through which it earns fees on substantially similar or identical investments across multiple funds, further increasing the economic benefits derived from its relationship with OTF.

125. These fall-out benefits, including direct administrative fees, expense reimbursements, shared platform efficiencies, and affiliated investment opportunities, materially increase the economic value of the advisory relationship to Defendant beyond the excessive advisory fees themselves.

| 4. | Gartenberg Factor 4: Economies of Scale are Not Shared with Investors |

126. Economies of scale in the provision of advisory services arise from the fact that as AUM increases, the marginal cost of providing advisory services for the assets decreases.

34

| Provided by CourtAlert | www.CourtAlert.com |

127. The legislative history of Section 36(b) recognizes that an investment adviser’s failure to pass on economies of scale to the fund is a principal cause of excessive fees:

It is noted . . . that problems arise due to the economies of scale attributable to the dramatic growth of the mutual fund industry. In some instances these economies of scale have not been shared with investors. Recently there has been a desirable tendency of the part of some fund managers to reduce their effective charges as the fund grows in size. Accordingly, the best industry practice will provide a guide.33

128. From 2021 to 2025, OTF’s portfolio assets increased by approximately 134%, from $6.1 billion to $14.3 billion.

129. The work required to operate a mutual fund or BDC does not increase proportionately with the assets under management. The economics of investment advisory services are widely understood to exhibit a downward-sloping average cost curve, in which the marginal cost of managing additional assets declines as assets increase, resulting in lower per-unit costs at scale. While initial and fixed operating costs for provision of investment advisory services are substantial (e.g., salaries for research, trading, and portfolio management personnel sufficient to manage an entire portfolio; office space; procurement of systems and information necessary to conduct research and manage the portfolio), the variable costs associated with managing additional AUM are generally much smaller on a relative basis and do not increase proportionately with asset growth.

130. Moreover, OTF’s investment goal, principal investment strategies and investment process have all remained the same since OTF was formed. Thus, notwithstanding the growth in OTF’s portfolio assets and Defendant’s advisory fees, the work facing Defendant has stayed fundamentally constant: it faces the same universe of possible investment securities, to which it applies the same techniques and strategies in pursuit of the same ends.

| 33 | See S. Rep. No. 91–184, 1970 U.S.C.C.A.N. 4897, 4901-02. |

35

| Provided by CourtAlert | www.CourtAlert.com |

131. Further, while it is true that OTF’s assets nearly doubled following the merger, OTF and OTF II had a massive investment overlap, with approximately 84% of OTF II’s investments also held in OTF, both funds employed the exact same investment strategy and Defendant co-invested substantially the same assets following OTF II’s inception.34 Thus, any “additional” work facing Defendant following the merger was minimal, at best.

132. Moreover, the March 2025 merger with OTF II (for which Defendant served as the investment advisor) that brought $5.56 billion of OTF II investments onto OTF’s book materially increased scale. And because the fee schedule following the merger carried no breakpoint, the stockholders did not share the scale of economies.

133. Because advisory fees are based upon OTF’s gross assets, portfolio asset increases necessarily increase the advisory fees. As a result of OTF’s increase in portfolio assets, the investment advisory fees paid by OTF to Defendant has also increased.

134. The aggregate amount of management and incentive fees that OTF has paid to Defendant has increased by 191% over the last five years, from $95 million in 2021 to $276 million in 2025. During that same timeframe, OTF’s total assets increased by 134% (largely as a result of the OTF II merger in March 2025). In other words, Defendant’s advisory fee increase (of 191%) was considerably disproportionate to the asset increase (of 134%). And while Defendant agreed to waive approximately $227,700 in fees in connection with the merger, that waiver was not only minimal relative to its total advisory fee in 2025 ($238 million), but also cosmetic relative to the permanent fee increase the merger produced in light of the fact that the asset base roughly doubled and Defendants’ fees are based on gross assets.

| 34 | See Blue Owl Technology Finance Corp., Form 425 (Nov. 14, 2024 transcript of webcast to discussed proposed merger of OTF and OTF II (filed on Nov. 14, 2024), available at https://www.sec.gov/Archives/edgar/data/1747777/000119312524258794/d835027d425.htm. |

36

| Provided by CourtAlert | www.CourtAlert.com |

135. Thus, because the variable costs associated with managing additional AUM are generally much smaller on a relative basis and do not increase proportionately with asset growth, OTF’s sizeable growth has generated substantial economies of scale for Defendant in connection with the investment advisory services provided to OTF.

136. Defendant has retained the lion’s share of such benefits for itself, rather than sharing those benefits with OTF’s stockholders.

137. As a result, the advisory fees that Defendant charges to, and receives from, OTF are grossly disproportionate to the investment advisory services provided, are excessive, and constitute a breach of Defendant’s fiduciary duties to OTF.

| 5. | Gartenberg Factor 5: Comparable Fee Structures—the Adviser’s Incentive Fee Structure Magnifies Asymmetry |

138. BDCs that are managed by investment advisers typically pay advisory fees ranging from 1% to 2% of the fund’s gross assets annually, and incentive fees are typically a percentage of the BDC’s profits, ranging from 17.5% to 20%.35

139. While the fee structure set forth in OTF’s Advisory Agreement falls within the range of advisory fees comparable to other BDCs, it does not include a typical clawback feature for incentive fees that are paid on deferred income that is not ultimately realized by OTF.

| 35 | See Publicly Traded Business Development Companies (BDCs): Investor Bulletin, INVESTOR.GOV, U.S.

SECURITIES AND EXCHANGE COMMISSION (Dec. 13, 2024), available at

https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-bulletins/publicly-traded-business-development-companies-bdcs-investor-bulletin; Business Development Companies (BDCs)

Frequently Asked Questions, EAGLE GLOBAL (Oct. 2023), available at https://www.eagleglobal.com/wp-content/uploads/2023/10/BDC-FAQs-October-2023.pdf;

BDC Facts and Stats, MAYER BROWN (June 15, 2025), available at

https://www.mayerbrown.com/-/media/files/perspectives-events/publications/2025/06/bdc-—factsstats-(2025).pdf%3Frev= |

37

| Provided by CourtAlert | www.CourtAlert.com |

140. Based on an analysis of 43 publicly traded BDCs, half of those BDCs’ advisory fee structures included a look-back feature, or clawback, that requires the adviser to return incentive fees that are based on deferred income, such as PIK interest, to account for credit losses.36 This clawback feature is a mechanism designed to ensure that compensation reflects full-cycle investment performance rather than interim or unrealized results, and that advisers are not rewarded for short-term income that later turns into long-term capital losses. This type of clawback mechanism is particularly important where incentive fees are calculated and paid on a quarterly basis based on accrued or non-cash income, as it aligns compensation with realized performance over the life of the investment, consistent with practices commonly observed in institutional investment structures.

141. This is a meaningful component of the advisory fee structure, as approximately $7.4 million of Defendant’s fees in the first quarter 2026 were attributable to PIK income.